How Much Is Car Insurance for a 19-year-old?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance for a 19-Year-Old?

- 4 Average Car Insurance Rates for 19-Year-Olds

- 5 Why Is Car Insurance So Expensive for 19-Year-Olds?

- 6 Factors That Affect Car Insurance Rates for Young Drivers

- 7 How to Lower Car Insurance Costs as a 19-Year-Old

- 8 Common Mistakes 19-Year-Olds Make with Car Insurance

- 9 Conclusion: Smart Choices Lead to Savings

- 10 Frequently Asked Questions

Car insurance for a 19-year-old is typically more expensive due to limited driving experience and higher risk. However, by choosing the right coverage, maintaining good grades, and shopping around, young drivers can reduce their premiums significantly.

Key Takeaways

- Young drivers pay more: 19-year-olds often face the highest insurance rates due to inexperience and higher accident likelihood.

- Location matters: Urban areas with heavy traffic and higher theft rates usually mean higher premiums than rural zones.

- Vehicle type impacts cost: Sports cars and luxury vehicles cost more to insure than safe, economical models.

- Good grades can save money: Many insurers offer discounts for students with a B average or higher.

- Defensive driving courses help: Completing an approved course may qualify you for a discount with some providers.

- Shop around annually: Comparing quotes from multiple insurers can uncover significant savings.

- Consider usage-based insurance: Programs that track safe driving habits can lead to lower rates over time.

📑 Table of Contents

- How Much Is Car Insurance for a 19-Year-Old?

- Average Car Insurance Rates for 19-Year-Olds

- Why Is Car Insurance So Expensive for 19-Year-Olds?

- Factors That Affect Car Insurance Rates for Young Drivers

- How to Lower Car Insurance Costs as a 19-Year-Old

- Common Mistakes 19-Year-Olds Make with Car Insurance

- Conclusion: Smart Choices Lead to Savings

How Much Is Car Insurance for a 19-Year-Old?

If you’re a 19-year-old getting behind the wheel for the first time—or even if you’ve been driving for a couple of years—you’ve probably noticed that car insurance doesn’t come cheap. In fact, it’s one of the biggest expenses new drivers face. But why is it so expensive? And more importantly, what can you do about it?

Let’s be real: at 19, you’re still considered a high-risk driver by most insurance companies. Statistically, young drivers—especially males under 25—are more likely to get into accidents, speed, or drive distracted. That means insurers charge higher premiums to offset the increased likelihood of claims. But that doesn’t mean you’re stuck paying sky-high rates forever. With smart decisions, good habits, and a little research, you can find affordable coverage that fits your budget.

In this guide, we’ll break down exactly how much car insurance costs for a 19-year-old, what factors influence those prices, and—most importantly—how you can lower your monthly bill. Whether you’re buying your first car or just trying to understand your family’s policy, this article will give you the tools to make informed choices.

Average Car Insurance Rates for 19-Year-Olds

Visual guide about How Much Is Car Insurance for a 19-year-old?

Image source: candsins.com

So, what’s the real number? How much is car insurance for a 19-year-old on average?

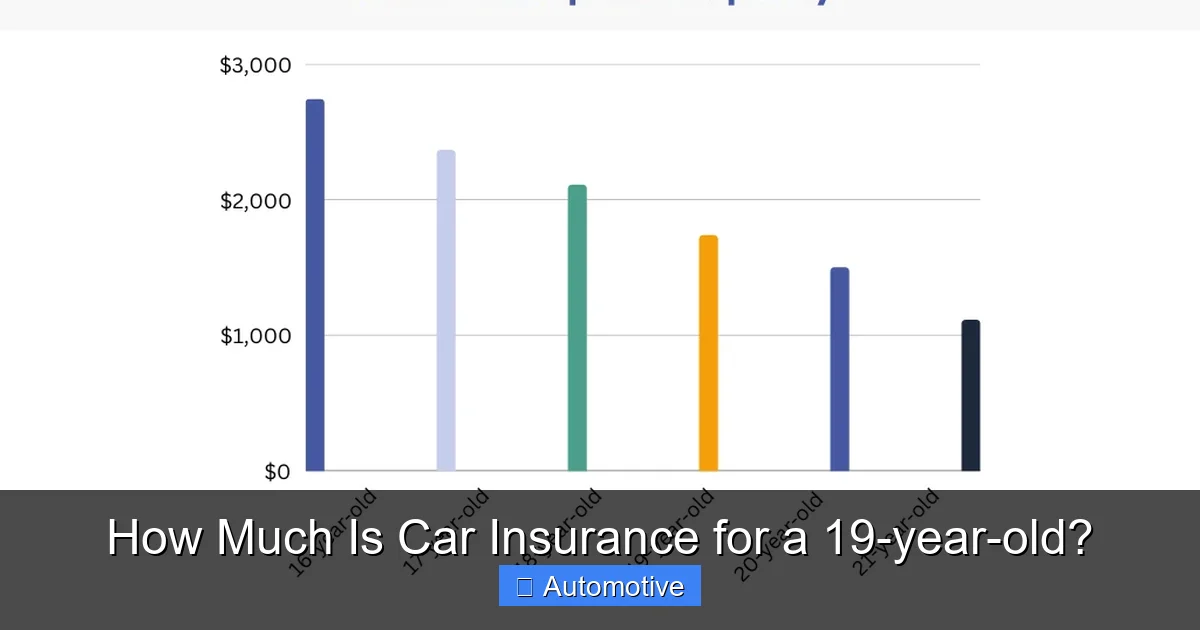

According to recent data from sources like the National Association of Insurance Commissioners (NAIC) and consumer research firms, the average annual cost of car insurance for a 19-year-old driver ranges from $2,500 to $4,500 per year. That’s roughly $200 to $375 per month—a huge chunk of change, especially if you’re working part-time or still in school.

To put that in perspective, a 35-year-old with a clean driving record might pay around $1,200 to $1,800 annually for the same coverage. That’s less than half what a 19-year-old pays. The gap is even wider for male teens, who typically pay 10–20% more than their female counterparts due to higher accident rates.

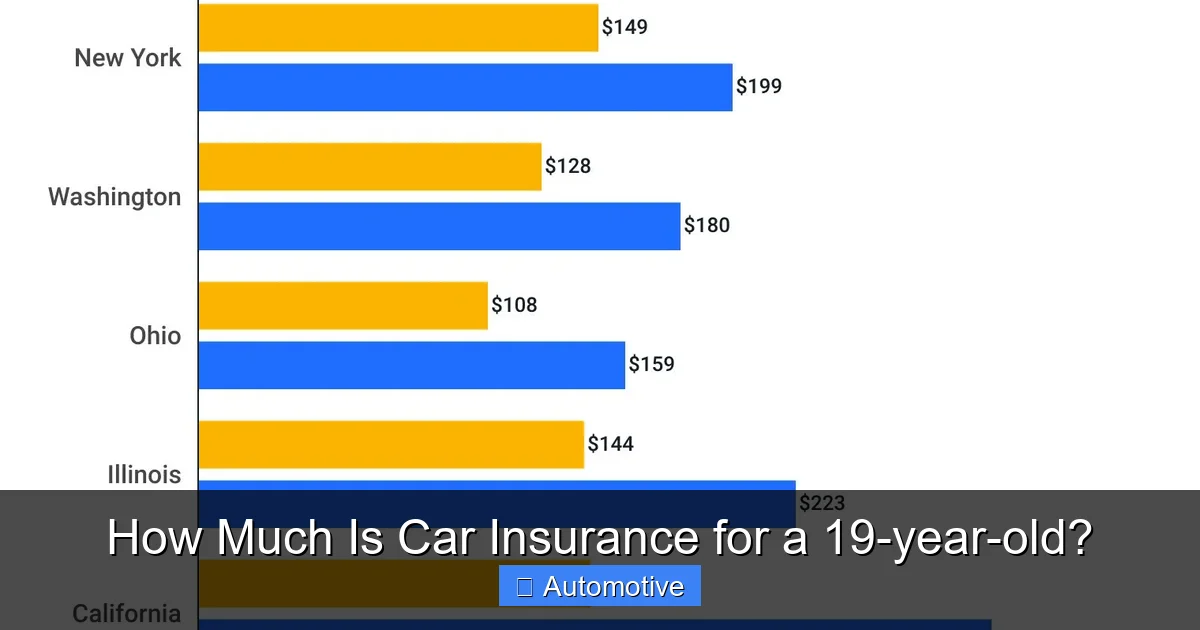

But these are just averages. Your actual rate could be higher or lower depending on where you live, what you drive, and your personal driving history. For example, a 19-year-old in Michigan might pay over $5,000 a year due to the state’s no-fault insurance laws and high medical coverage requirements. Meanwhile, someone in Maine or Ohio might pay closer to $2,000.

Breaking Down the Numbers by Gender and Location

Let’s look at some real-world examples. A 19-year-old male in California with a clean record and a mid-size sedan might pay around $3,800 per year for full coverage. A female of the same age, driving the same car in the same state, might pay about $3,200. That’s a $600 difference—just for being a different gender.

Location plays an even bigger role. In Florida, where hurricanes, traffic congestion, and high theft rates are common, premiums can soar. A 19-year-old in Miami might pay $4,500 or more. In contrast, a rural driver in North Dakota might pay under $2,200.

These numbers show that while age is a major factor, it’s not the only one. Your zip code, vehicle, and even your credit score (in states where it’s allowed) can shift your rate up or down.

Full Coverage vs. Minimum Coverage

Another key factor is the type of coverage you choose. Most 19-year-olds are advised to get full coverage—liability, collision, and comprehensive—especially if they’re financing or leasing a car. But full coverage is expensive.

For a 19-year-old, full coverage averages around $3,500 to $4,500 per year. Minimum liability coverage—just what’s required by law—might cost $1,500 to $2,500. While that sounds tempting, skimping on coverage can leave you vulnerable. If you cause an accident, liability only covers the other person’s damages—not your car, medical bills, or lost wages.

For example, if you total a $20,000 car and only have liability, you’re on the hook for the full repair or replacement cost. That’s why many financial experts recommend full coverage for young drivers, at least until the car is paid off or significantly depreciated.

Why Is Car Insurance So Expensive for 19-Year-Olds?

Visual guide about How Much Is Car Insurance for a 19-year-old?

Image source: res.cloudinary.com

Now that you know the average cost, let’s dig into why it’s so high. Insurance companies use complex algorithms to assess risk, and for 19-year-olds, the data isn’t in their favor.

Statistical Risk and Inexperience

The biggest reason? Inexperience. According to the Insurance Institute for Highway Safety (IIHS), drivers aged 16 to 19 are nearly three times more likely to be in a fatal crash than drivers over 20. At 19, you’re still in that high-risk group, even if you’ve been driving for a few years.

Why? New drivers are more likely to:

– Speed or drive aggressively

– Be distracted by phones, passengers, or music

– Misjudge distances or traffic conditions

– Drive at night or in bad weather without proper skills

Insurance companies see these patterns and adjust premiums accordingly. It’s not personal—it’s actuarial science. They’re covering their bets based on what the data says.

Gender Differences in Premiums

You might have noticed that male teens usually pay more. That’s because, statistically, young men are involved in more accidents, especially severe ones. The IIHS reports that male drivers aged 16–19 have crash rates nearly twice as high as female drivers in the same age group.

This gap starts to close around age 25, when driving habits mature. But at 19, the difference is still significant. Some states, like California and Hawaii, have banned gender-based pricing, but in most places, it’s still a factor.

The Role of Credit and Education

In many states, insurers also consider your credit score when setting rates. Young drivers often have limited or no credit history, which can be interpreted as a risk factor. A low score might bump your premium by hundreds of dollars.

Similarly, your education level can matter. Some companies offer discounts for students who maintain a B average or higher—proof that you’re responsible and focused. It’s a small perk, but every dollar counts.

Factors That Affect Car Insurance Rates for Young Drivers

Visual guide about How Much Is Car Insurance for a 19-year-old?

Image source: forbes.com

Beyond age and gender, several other factors influence how much you’ll pay for car insurance. Understanding these can help you make smarter choices and potentially lower your costs.

1. Where You Live

Your location is one of the biggest determinants of your premium. Urban areas with high traffic, crime, and accident rates—like New York City, Los Angeles, or Chicago—typically have the highest insurance costs. Rural areas, with less traffic and lower theft rates, are usually cheaper.

For example, a 19-year-old in Los Angeles might pay $4,200 a year, while someone in a small town in Iowa might pay $2,100. Even within the same state, rates can vary widely. Living in a high-theft neighborhood or near a busy highway can increase your risk profile.

2. The Car You Drive

The type of vehicle you insure makes a huge difference. Sports cars, luxury vehicles, and models with high repair costs are expensive to insure. Why? They’re more likely to be stolen, cost more to fix, and are often driven aggressively.

On the other hand, safe, reliable, and economical cars—like a Honda Civic, Toyota Corolla, or Subaru Impreza—are cheaper to insure. These models often come with advanced safety features like automatic emergency braking, lane departure warnings, and blind-spot monitoring, which can qualify you for discounts.

For example, insuring a 2020 Ford Mustang might cost $4,000 a year for a 19-year-old, while a 2020 Honda Civic could be under $2,800. That’s a $1,200 difference—just for choosing a different car.

3. Driving Record and Claims History

Even at 19, your driving record matters. A clean record with no accidents or tickets will help keep your rates lower. But one speeding ticket or at-fault accident can increase your premium by 20–50%.

For instance, a single at-fault accident might raise your annual premium from $3,000 to $4,500. A DUI? That could double your rate or even get you dropped by your insurer.

The good news? Some insurers offer accident forgiveness programs, and tickets may fall off your record after a few years. But until then, every mistake costs you.

4. Coverage Level and Deductible

The more coverage you buy, the more you’ll pay. Full coverage includes liability, collision, and comprehensive, while minimum coverage only meets state requirements.

You can also adjust your deductible—the amount you pay out of pocket before insurance kicks in. A higher deductible (like $1,000 instead of $500) lowers your premium but increases your financial risk if you get into an accident.

For a 19-year-old, a $500 deductible might add $200–$300 to your annual premium compared to a $1,000 deductible. It’s a trade-off: pay more now for lower monthly costs, or pay less upfront but risk a big bill later.

5. Discounts and Savings Opportunities

The bright side? There are plenty of ways to save. Many insurers offer discounts specifically for young drivers. Here are some of the most common:

– Good Student Discount: Maintain a B average or higher and save 10–25%.

– Defensive Driving Course: Complete an approved course and qualify for a discount (usually 5–10%).

– Low Mileage Discount: Drive less than 7,500–10,000 miles per year? You might qualify.

– Usage-Based Insurance: Use a telematics app or device to track your driving. Safe habits = lower rates.

– Multi-Policy Discount: Bundle your car insurance with renters or home insurance.

– Pay-in-Full Discount: Pay your annual premium upfront instead of monthly.

For example, a 19-year-old with good grades, a clean record, and a usage-based program might save $800–$1,200 a year compared to the average rate.

How to Lower Car Insurance Costs as a 19-Year-Old

Now for the good part: how to actually reduce your insurance bill. While you can’t change your age (yet!), there are plenty of strategies to make coverage more affordable.

1. Stay on Your Parents’ Policy

One of the easiest ways to save is by staying on your parents’ insurance policy. Most insurers allow young drivers to be added as a secondary driver, which is usually much cheaper than getting your own policy.

For example, adding a 19-year-old to a family plan might increase the premium by $1,500–$2,500 per year. But buying a standalone policy could cost $3,500–$4,500. That’s a savings of $1,000–$2,000.

Just make sure you’re listed as a occasional or secondary driver—not the primary operator—unless you’re the main driver of the car.

2. Choose a Safe, Affordable Car

As we mentioned earlier, your vehicle choice has a big impact. Avoid high-performance cars, luxury brands, and models with high theft rates. Instead, opt for:

– Compact sedans with high safety ratings

– Cars with advanced driver-assistance systems (ADAS)

– Models with low repair and replacement costs

Check the Insurance Institute for Highway Safety (IIHS) or National Highway Traffic Safety Administration (NHTSA) for safety ratings before buying.

3. Maintain Good Grades

Many insurers offer a good student discount for full-time students under 25 with a B average or higher. You’ll usually need to provide a report card or transcript once a year.

This discount can save you 10–25%, which on a $3,500 policy, is $350–$875 per year. That’s free money just for doing well in school.

4. Take a Defensive Driving Course

Completing an approved defensive driving course can improve your skills and qualify you for a discount. These courses teach hazard recognition, safe braking, and accident avoidance.

Most insurers offer a 5–10% discount, and some states even reduce points on your license if you get a ticket. Look for courses certified by your state’s DMV or approved by major insurers like State Farm or GEICO.

5. Use Telematics or Usage-Based Insurance

Telematics programs like Progressive’s Snapshot, Allstate’s Drivewise, or State Farm’s Drive Safe & Save monitor your driving habits through a smartphone app or plug-in device.

They track:

– Hard braking and acceleration

– Speed

– Time of day you drive

– Mileage

If you drive safely—especially during low-risk hours—you can earn discounts of 10–30%. Some programs even offer instant feedback to help you improve.

For a 19-year-old, this can be a game-changer. It turns your driving behavior into savings, proving that you’re not a high-risk driver.

6. Shop Around Every Year

Insurance companies don’t always reward loyalty. In fact, some raise rates over time unless you negotiate. That’s why it’s smart to compare quotes from at least three insurers every year.

Use online comparison tools like NerdWallet, The Zebra, or Insurify to get personalized quotes. You might find a better deal with a regional insurer or a company that specializes in young drivers.

For example, a 19-year-old in Texas might pay $3,800 with one company but only $2,900 with another—just by switching.

7. Consider Increasing Your Deductible

Raising your deductible from $500 to $1,000 can reduce your premium by 15–30%. For a $3,500 policy, that’s $525–$1,050 in savings.

Just make sure you can afford the higher out-of-pocket cost if you need to file a claim. Keep the deductible amount in a savings account just in case.

Common Mistakes 19-Year-Olds Make with Car Insurance

Even with the best intentions, young drivers often make costly mistakes when it comes to insurance. Here are a few to avoid:

1. Lying on Your Application

It might be tempting to say you’re the primary driver of your parents’ car or that you have more experience than you do. But lying on your insurance application is fraud—and it can get your policy canceled or claims denied.

Insurers verify information through DMV records, credit reports, and even social media. If they find out you lied, you could face fines, legal trouble, or difficulty getting coverage in the future.

2. Skimping on Coverage

It’s understandable to want the cheapest option, but minimum coverage can leave you exposed. If you cause a serious accident, liability limits might not cover all the damages—leaving you personally responsible for thousands of dollars.

Full coverage might cost more upfront, but it protects your assets and gives you peace of mind.

3. Ignoring Discounts

Many young drivers don’t realize how many discounts are available. Failing to ask about good student, defensive driving, or telematics discounts means leaving money on the table.

Always ask your insurer: “What discounts am I eligible for?” You might be surprised.

4. Not Updating Your Policy

Life changes—and so should your insurance. If you move, change schools, get a job, or improve your grades, update your policy. You might qualify for new discounts or need to adjust coverage.

For example, moving from a city to a rural area could lower your rate by 20%. Not updating your address means you’re overpaying.

Conclusion: Smart Choices Lead to Savings

So, how much is car insurance for a 19-year-old? On average, between $2,500 and $4,500 per year—but that number isn’t set in stone. With the right strategies, you can significantly reduce your costs and build a foundation for affordable coverage as you get older.

The key is to be proactive. Choose a safe car, maintain good grades, drive responsibly, and take advantage of every discount available. Stay on your parents’ policy if possible, and always shop around for the best deal.

Remember, insurance isn’t just a legal requirement—it’s protection. It shields you from financial disaster if something goes wrong. And while the cost might seem high now, it gets better with time. Every year you drive safely, your risk profile improves, and your rates will likely go down.

So don’t let high premiums discourage you. With smart choices and a little effort, you can get the coverage you need at a price you can afford. Your future self will thank you.

Frequently Asked Questions

How much is car insurance for a 19-year-old on average?

Car insurance for a 19-year-old typically costs between $2,500 and $4,500 per year, or $200 to $375 per month. Rates vary by location, vehicle, and driving history.

Why is car insurance so expensive for 19-year-olds?

Insurance is expensive because young drivers are statistically more likely to be in accidents. Inexperience, higher risk-taking behavior, and lack of driving history contribute to higher premiums.

Can a 19-year-old get a discount on car insurance?

Yes! Many insurers offer discounts for good grades, defensive driving courses, low mileage, and usage-based programs. These can save hundreds of dollars per year.

Should a 19-year-old get full coverage or minimum coverage?

Full coverage is recommended, especially if the car is financed or valuable. It protects your vehicle and assets, while minimum coverage only meets legal requirements.

Does staying on my parents’ insurance save money?

Yes, adding a 19-year-old to a family policy is usually cheaper than buying a standalone plan. It can save $1,000 or more per year.

Will my car insurance rate go down as I get older?

Yes, rates typically decrease significantly after age 25 as you gain more driving experience and move into a lower-risk category. Safe driving habits also help reduce costs over time.