Which State Has the Highest Car Insurance Rates?

Louisiana currently holds the title for the highest car insurance rates in the U.S., with average annual premiums exceeding $3,000. High accident rates, severe weather, and state regulations all contribute to these steep costs, but drivers can still find savings with smart shopping and safety measures.

Key Takeaways

- Louisiana has the highest car insurance rates: Drivers pay an average of over $3,000 per year, far above the national average.

- Multiple factors influence premiums: Accident frequency, weather risks, population density, and state laws all play a role.

- No-fault states tend to have higher rates: These states require personal injury protection (PIP), increasing overall costs.

- Weather disasters drive up claims: Hurricanes, floods, and hailstorms in states like Florida and Louisiana lead to more expensive policies.

- Urban areas cost more than rural ones: High traffic and theft rates in cities like Detroit and Miami push premiums higher.

- You can lower your rates: Safe driving, good credit, and comparing quotes can help reduce costs regardless of location.

- Minimum coverage isn’t always cheapest: While it meets legal requirements, full coverage may offer better long-term value.

📑 Table of Contents

Which State Has the Highest Car Insurance Rates?

If you’ve ever shopped for car insurance, you’ve probably noticed that prices can vary wildly depending on where you live. A driver in Maine might pay less than $1,000 a year, while someone in Louisiana could be shelling out over $3,000. So, which state has the highest car insurance rates? The answer isn’t just about geography—it’s a mix of weather, laws, population, and even crime rates.

Understanding why car insurance costs differ so much across states can help you make smarter decisions about coverage, whether you’re moving, buying a new car, or just trying to save money. In this guide, we’ll break down the top states with the highest premiums, explore the reasons behind these costs, and share practical tips to help you keep your own rates as low as possible.

Top 5 States with the Highest Car Insurance Rates

Visual guide about Which State Has the Highest Car Insurance Rates?

Image source: arizent.brightspotcdn.com

When it comes to car insurance, not all states are created equal. Some consistently rank at the top for the most expensive premiums, and Louisiana leads the pack by a wide margin. Let’s take a closer look at the five states where drivers pay the most for coverage.

1. Louisiana – The Most Expensive State

Louisiana holds the unfortunate title of the state with the highest car insurance rates in the U.S. In 2024, the average annual premium for full coverage in Louisiana is over $3,000—nearly double the national average. That’s a staggering number, especially when you consider that many drivers in other states pay less than half that amount.

So, what makes Louisiana so expensive? Several factors come into play. First, the state has a high rate of uninsured drivers—around 14%, which is well above the national average of about 12%. When more drivers are uninsured, those who do carry coverage end up paying more to cover the risks.

Second, Louisiana is prone to severe weather, especially hurricanes and flooding. These natural disasters lead to a high volume of claims, from vehicle damage to total losses. Insurance companies pass these costs on to policyholders in the form of higher premiums.

Finally, the state’s legal environment plays a role. Louisiana is a “fault” state, meaning the driver at fault in an accident is responsible for damages. This can lead to more lawsuits and higher payouts, especially in densely populated areas like New Orleans.

2. Florida – High Claims and Hurricane Risk

Coming in second is Florida, where the average annual premium hovers around $2,800. Like Louisiana, Florida faces significant weather-related risks. Hurricanes, tropical storms, and flooding are common, especially along the Gulf and Atlantic coasts. These events result in thousands of vehicle damage claims each year.

But weather isn’t the only culprit. Florida also has a high rate of uninsured drivers—about 20%, one of the highest in the nation. This puts additional financial pressure on insurers and, in turn, on policyholders.

Another factor is the state’s no-fault insurance system. Florida requires drivers to carry Personal Injury Protection (PIP) coverage, which pays for medical expenses regardless of who caused the accident. While this system is designed to reduce lawsuits, it can also lead to fraud and inflated claims, driving up costs for everyone.

3. Michigan – The No-Fault State with Unlimited PIP

Michigan ranks third, with average premiums around $2,700 per year. The state’s unique no-fault insurance system is a major reason for the high costs. Michigan requires drivers to carry unlimited Personal Injury Protection (PIP) coverage, meaning medical bills are covered no matter how high they go.

While this provides excellent protection for injured drivers, it also leads to some of the highest medical costs in the country. Hospitals and clinics often charge more because they know insurers will pay. Additionally, fraud and abuse in the PIP system have been ongoing issues, further inflating premiums.

In 2021, Michigan passed reforms to lower costs, including allowing drivers to choose lower PIP limits. However, many drivers still opt for full coverage, keeping overall rates high.

4. New York – Urban Density and High Claims

New York comes in fourth, with average annual premiums around $2,600. The state’s high population density, especially in New York City, contributes to more traffic, accidents, and vehicle theft. Urban areas are inherently riskier for insurers, leading to higher premiums.

New York is also a no-fault state, requiring PIP coverage. Like Florida and Michigan, this increases the cost of claims. Additionally, the state has strict insurance regulations and high litigation rates, which can drive up administrative costs for insurers.

Another factor is the high cost of living. Everything from repairs to medical care is more expensive in New York, and those costs are reflected in insurance premiums.

5. Nevada – Rapid Growth and Rising Claims

Rounding out the top five is Nevada, where average premiums are around $2,500 per year. The state has seen rapid population growth, especially in Las Vegas and Reno. More drivers on the road mean more accidents and claims.

Nevada also has a high rate of vehicle theft, particularly in urban areas. According to the FBI, Las Vegas consistently ranks among the top cities for car theft in the U.S. Insurers factor this risk into their pricing, leading to higher premiums.

Additionally, Nevada is a no-fault state, requiring PIP coverage. While the limits are lower than in Michigan, the combination of theft, accidents, and population growth keeps costs elevated.

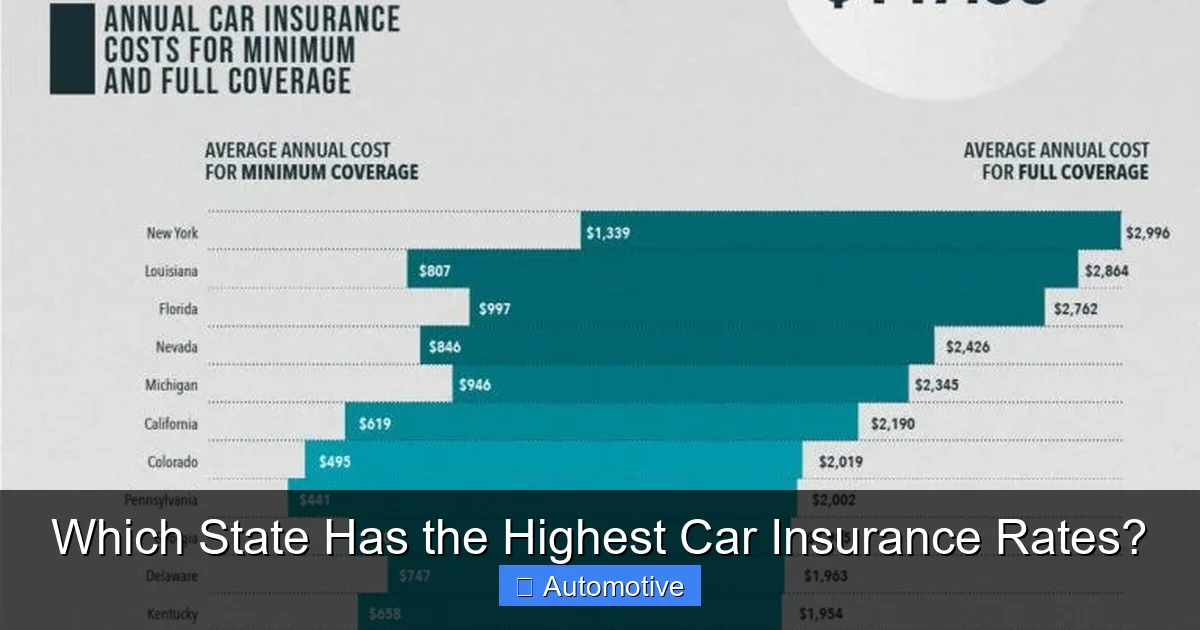

Why Do Car Insurance Rates Vary So Much by State?

Visual guide about Which State Has the Highest Car Insurance Rates?

Image source: best-infographics.com

Now that we’ve identified the states with the highest car insurance rates, it’s important to understand why these differences exist. Insurance companies use complex algorithms to assess risk, and location is one of the biggest factors. Here are the key reasons why premiums vary so much from one state to another.

State Laws and Insurance Requirements

Every state sets its own rules for car insurance, and these laws have a direct impact on premiums. For example, no-fault states like Florida, Michigan, and New York require drivers to carry Personal Injury Protection (PIP) coverage. This means your own insurance pays for your medical bills after an accident, regardless of who was at fault.

While this system is designed to reduce lawsuits and speed up claims, it can also lead to higher costs. Medical expenses add up quickly, and insurers pass those costs on to consumers. In states with unlimited PIP, like Michigan, the financial burden is especially high.

On the other hand, states with “fault” or “tort” systems allow injured parties to sue the at-fault driver for damages. This can lead to more litigation, but it may also keep premiums lower in some cases—though not always.

Minimum coverage requirements also vary. Some states require only liability insurance, while others mandate additional coverage like PIP or uninsured motorist protection. The more coverage required, the higher the premium.

Weather and Natural Disasters

Weather plays a huge role in car insurance costs. States prone to hurricanes, tornadoes, floods, or hailstorms see more vehicle damage claims, which drives up premiums.

For example, Louisiana and Florida are both in hurricane-prone regions. When a major storm hits, thousands of cars can be damaged or destroyed. Insurers pay out massive claims, and those costs are spread across all policyholders in the state.

Similarly, states like Oklahoma and Kansas face frequent tornadoes, while Arizona and Colorado deal with severe hailstorms. Even winter storms in the Midwest and Northeast can lead to increased claims from accidents and vehicle damage.

Insurance companies use historical weather data to predict future risks. If a state has a history of severe weather, premiums will reflect that risk.

Population Density and Urban vs. Rural Areas

Where you live within a state also matters. Urban areas tend to have higher insurance rates than rural ones. Why? More people mean more traffic, more accidents, and a higher chance of theft or vandalism.

For example, drivers in Detroit, Michigan, or Miami, Florida, pay significantly more than those in smaller towns in the same states. High population density increases the likelihood of collisions, and urban areas often have higher rates of vehicle theft and insurance fraud.

Rural areas, by contrast, have fewer cars on the road and lower crime rates. This reduces the risk for insurers, leading to lower premiums. However, rural drivers may face longer response times after an accident, which can affect claim processing.

Accident and Crime Rates

States with higher accident rates naturally have higher insurance costs. More accidents mean more claims, and insurers adjust premiums accordingly.

But it’s not just about accidents. Crime rates—especially vehicle theft and insurance fraud—also play a role. States like Nevada and Florida have high rates of car theft, which increases the risk for insurers.

Insurance fraud is another concern. In some states, staged accidents or exaggerated injury claims are common. These fraudulent activities cost insurers millions each year, and those costs are passed on to honest policyholders.

Cost of Living and Repair Expenses

The cost of living in a state affects everything from medical care to car repairs—and that includes insurance. In states with high living costs, like New York or California, labor and parts are more expensive. This means repairs cost more, and medical bills are higher.

Insurance companies factor these costs into their pricing. If it costs more to fix a car or treat an injury in a particular state, premiums will be higher to cover those expenses.

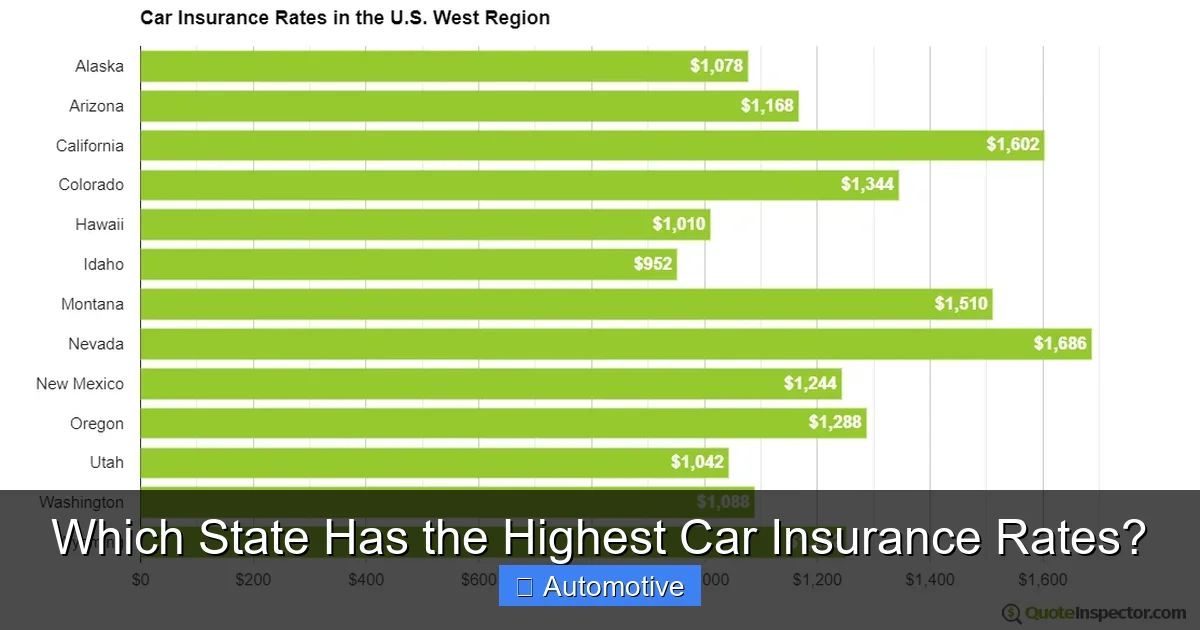

How to Lower Your Car Insurance Rates

Visual guide about Which State Has the Highest Car Insurance Rates?

Image source: quoteinspector.com

Even if you live in a state with high car insurance rates, there are ways to reduce your premiums. While you can’t change your location, you can take steps to lower your risk profile and save money.

Shop Around and Compare Quotes

One of the best ways to save is to shop around. Insurance rates can vary significantly between companies, even within the same state. Getting quotes from at least three different insurers can help you find the best deal.

Use online comparison tools or work with an independent agent who can access multiple carriers. Don’t just look at the price—also consider coverage options, customer service, and claims handling.

Maintain a Clean Driving Record

Your driving history has a major impact on your rates. Accidents, speeding tickets, and DUIs can all lead to higher premiums. On the other hand, a clean record can qualify you for safe driver discounts.

Many insurers offer accident forgiveness programs, which prevent your rates from increasing after your first accident. Some also offer defensive driving courses that can reduce your premium.

Improve Your Credit Score

In most states, insurers use credit-based insurance scores to help determine premiums. Drivers with higher credit scores are seen as lower risk and often pay less.

To improve your credit, pay bills on time, reduce debt, and check your credit report for errors. Even a small improvement in your score can lead to lower rates.

Choose the Right Coverage

While it’s tempting to go with the minimum coverage to save money, it may not be the best choice in the long run. Minimum coverage often leaves you underinsured, especially in high-cost states.

Consider your vehicle’s value and your financial situation. If you drive an older car, you might skip collision and comprehensive coverage. But if you have a newer vehicle or live in a high-risk area, full coverage may be worth the extra cost.

Take Advantage of Discounts

Most insurers offer a variety of discounts. Common ones include:

- Multi-policy discounts (bundling auto and home insurance)

- Safe driver discounts

- Good student discounts

- Low-mileage discounts

- Anti-theft device discounts

Ask your insurer about available discounts and see which ones you qualify for.

Increase Your Deductible

Raising your deductible—the amount you pay out of pocket before insurance kicks in—can lower your premium. For example, increasing your deductible from $500 to $1,000 could save you 15–30% on your policy.

Just make sure you can afford the higher deductible if you need to file a claim.

The Impact of Technology and Telematics

Technology is changing the way insurers assess risk and set premiums. Many companies now offer usage-based insurance (UBI) programs that use telematics devices or smartphone apps to track your driving behavior.

These programs monitor things like speed, braking, acceleration, and mileage. Safe drivers can earn discounts of up to 20–30%, even in high-cost states.

For example, Progressive’s Snapshot program and State Farm’s Drive Safe & Save offer savings based on how you drive. If you’re a cautious driver, these programs can help offset high state premiums.

Conclusion

So, which state has the highest car insurance rates? Louisiana currently tops the list, with average annual premiums exceeding $3,000. Florida, Michigan, New York, and Nevada round out the top five, each with unique factors driving up costs.

While you can’t control where you live, you can take steps to lower your premiums. Shopping around, maintaining a clean driving record, and taking advantage of discounts can all help reduce your costs. And with the rise of telematics and usage-based insurance, safer drivers have more opportunities than ever to save.

Understanding the factors behind high insurance rates empowers you to make informed decisions. Whether you’re in a high-cost state or just looking to save, a little knowledge goes a long way.

Frequently Asked Questions

Why is car insurance so expensive in Louisiana?

Louisiana has high car insurance rates due to a combination of factors, including a high rate of uninsured drivers, frequent hurricanes and flooding, and a legal environment that leads to more lawsuits and claims. These risks drive up costs for insurers, which are passed on to policyholders.

Do no-fault states always have higher insurance rates?

Not always, but no-fault states like Florida, Michigan, and New York often have higher premiums because they require Personal Injury Protection (PIP) coverage. This increases claim costs, especially in states with unlimited PIP or high medical expenses.

Can I lower my car insurance if I live in a high-cost state?

Yes, you can still save money by shopping around, maintaining a clean driving record, improving your credit score, and taking advantage of discounts. Usage-based insurance programs can also help safe drivers reduce their premiums.

How does weather affect car insurance rates?

Severe weather like hurricanes, tornadoes, and hailstorms lead to more vehicle damage claims. Insurers factor in historical weather data when setting premiums, so states with frequent storms often have higher rates.

Is minimum coverage enough in high-cost states?

Minimum coverage meets legal requirements but may leave you underinsured, especially in states with high repair and medical costs. Consider your vehicle’s value and financial situation before deciding on coverage levels.

Do urban areas always have higher insurance rates than rural areas?

Generally, yes. Urban areas have more traffic, accidents, and theft, which increases risk for insurers. However, some rural areas with poor road conditions or high crime rates may also have elevated premiums.