What Happens If You Miss a Car Insurance Payment

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 What Happens If You Miss a Car Insurance Payment?

- 4 Immediate Consequences of Missing a Payment

- 5 Risks of Driving Without Insurance

- 6 How Insurers Handle Missed Payments

- 7 Long-Term Financial and Legal Impacts

- 8 How to Prevent Missing Payments in the Future

- 9 What to Do If You’ve Already Missed a Payment

- 10 Conclusion

- 11 Frequently Asked Questions

Missing a car insurance payment can lead to late fees, policy cancellation, and even legal trouble if you drive uninsured. Acting quickly—contacting your insurer, catching up on payments, or exploring grace periods—can help you get back on track and avoid long-term consequences.

Key Takeaways

- Late fees and interest charges: Most insurers add a fee if you miss a payment, increasing your total cost.

- Grace periods may apply: Many companies offer a short window (usually 7–15 days) to pay without penalty.

- Policy cancellation is possible: If you don’t pay within the grace period, your coverage can be canceled.

- Driving without insurance is illegal: In most states, driving uninsured can result in fines, license suspension, or vehicle impoundment.

- Reinstatement may require extra steps: Getting your policy back often involves back payments, fees, and sometimes a new application.

- Credit score impact: Unpaid insurance bills can be sent to collections, hurting your credit.

- Proactive communication helps: Calling your insurer early can lead to payment plans or temporary relief.

📑 Table of Contents

- What Happens If You Miss a Car Insurance Payment?

- Immediate Consequences of Missing a Payment

- Risks of Driving Without Insurance

- How Insurers Handle Missed Payments

- Long-Term Financial and Legal Impacts

- How to Prevent Missing Payments in the Future

- What to Do If You’ve Already Missed a Payment

- Conclusion

What Happens If You Miss a Car Insurance Payment?

We’ve all been there—life gets busy, bills pile up, and sometimes a due date slips through the cracks. Maybe you were traveling, dealing with an emergency, or simply forgot. Whatever the reason, missing a car insurance payment is more common than you might think. But while it might seem like a small oversight, the consequences can ripple through your finances, driving privileges, and peace of mind.

Car insurance isn’t just a monthly bill—it’s a legal requirement in almost every state. It protects you, your passengers, and other drivers on the road. When you sign up for a policy, you’re entering a contract with your insurer. That means paying on time is part of the deal. So what happens if you miss that payment? The short answer: it depends on your insurer, your state’s laws, and how quickly you act. But the longer answer involves late fees, potential cancellation, legal risks, and even damage to your credit score.

The good news? Most insurance companies understand that life happens. They don’t want to drop you immediately. Instead, they usually offer a grace period and may work with you to get things back on track. The key is to respond quickly. Ignoring the problem only makes it worse. In this guide, we’ll walk you through exactly what happens when you miss a car insurance payment, what your options are, and how to prevent it from happening again.

Immediate Consequences of Missing a Payment

Visual guide about What Happens If You Miss a Car Insurance Payment

Image source: tadvantagealpha-com.cdn-convertus.com

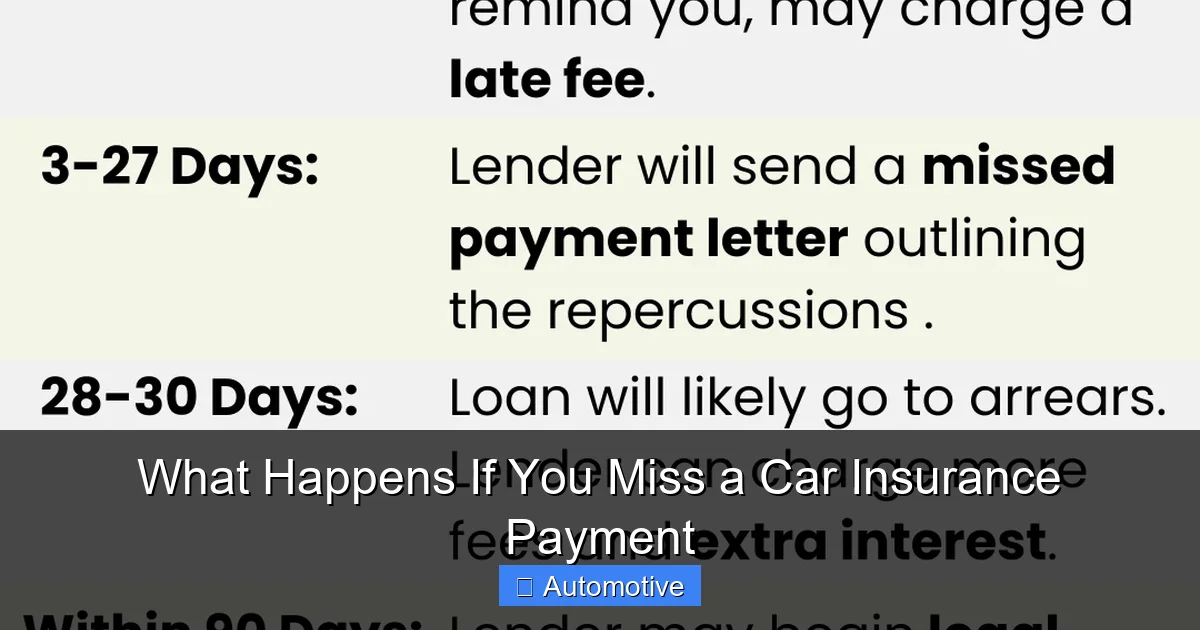

The moment your car insurance payment is due and doesn’t go through, your insurer takes notice. While they won’t cancel your policy right away, they will start the process of addressing the missed payment. Here’s what typically happens in the first few days.

Late Fees and Interest Charges

One of the first things you’ll face is a late fee. Most insurance companies charge between $10 and $50 for a missed payment, depending on your policy and state regulations. This fee is added to your next bill, so it compounds if you continue to delay.

For example, let’s say your monthly premium is $120, and you miss the due date. Your insurer adds a $25 late fee. Now your next payment is $145. If you miss that one too, another fee kicks in. Over time, these small charges can add up quickly.

Some insurers also charge interest on overdue balances, especially if your policy is financed through them (common with monthly payment plans). This means you’re not just paying for insurance—you’re paying extra for the privilege of paying late.

Grace Periods: Your Safety Net

The good news is that most insurers offer a grace period. This is a short window—usually between 7 and 15 days—after your due date during which you can pay without losing coverage. During this time, your policy remains active, and you can still file claims.

Grace periods vary by company and state. For instance, State Farm typically offers a 10-day grace period, while Geico may give you up to 14 days. Some states even mandate minimum grace periods by law. California, for example, requires a 10-day grace period for auto insurance.

It’s important to note that grace periods don’t eliminate late fees. You’ll still be charged, but your coverage stays intact. Think of it as a second chance—use it wisely.

Policy Status Changes

If you don’t pay within the grace period, your policy status changes. Your insurer will send you a notice—usually by mail or email—informing you that your policy is “lapsed” or “pending cancellation.” This means your coverage is no longer active, and you’re technically uninsured.

At this point, you’re at risk of legal and financial trouble. Driving without insurance is illegal in 49 states (New Hampshire is the only exception, and even there, financial responsibility laws apply). If you’re pulled over or involved in an accident, the consequences can be severe.

Risks of Driving Without Insurance

Visual guide about What Happens If You Miss a Car Insurance Payment

Image source: autodeal.com.ph

Driving without car insurance isn’t just risky—it’s illegal. And the penalties go far beyond a simple fine. Let’s break down what could happen if you’re caught behind the wheel without coverage.

Legal Penalties and Fines

Every state has its own penalties for driving uninsured, but they all include fines. These can range from $100 to over $1,000, depending on whether it’s your first offense or a repeat violation.

For example, in Texas, a first-time offense can cost you up to $350 in fines, plus court fees. In Florida, you could face a $500 fine and a suspended license. Repeat offenders often face higher fines and longer license suspensions.

License and Registration Suspension

In many states, driving without insurance leads to an automatic suspension of your driver’s license and vehicle registration. This means you can’t legally drive until you reinstate both.

Reinstating your license often requires paying a reinstatement fee (usually $50–$200), providing proof of insurance, and sometimes completing a defensive driving course. In some cases, you may need to file an SR-22 form—a document that proves you’re carrying the minimum required coverage.

Vehicle Impoundment

If you’re pulled over and found to be driving without insurance, your vehicle may be impounded. Getting it back involves paying towing and storage fees, which can cost hundreds of dollars. In some states, you’ll also need to show proof of insurance before the car is released.

Increased Insurance Rates in the Future

Even after you get your policy back, the damage isn’t over. Insurance companies view lapses in coverage as a red flag. When you apply for new coverage, you’ll likely be classified as a “high-risk” driver, which means higher premiums.

For example, a driver with continuous coverage might pay $100 a month. After a lapse, that same driver could see their rate jump to $150 or more. And if you have an accident during the lapse, the rate increase could be even steeper.

How Insurers Handle Missed Payments

Visual guide about What Happens If You Miss a Car Insurance Payment

Image source: legaladvice.org.za

Not all insurance companies handle missed payments the same way. Some are more lenient, while others take a strict approach. Understanding your insurer’s process can help you respond effectively.

Communication and Notices

When you miss a payment, your insurer will typically send a series of notices. The first is a reminder, usually sent a few days before the due date. If you miss it, they’ll send a late notice, followed by a cancellation warning if you don’t pay within the grace period.

These notices are often sent via email, text, or mail. Some insurers also call or send automated messages. It’s important to keep your contact information up to date so you don’t miss these alerts.

Automatic Payments and Payment Plans

Many insurers offer automatic payment options, which can prevent missed payments altogether. By linking your bank account or credit card, your premium is deducted on the due date each month. This is one of the easiest ways to avoid late fees and lapses.

If you’re struggling to pay, some companies offer payment plans or temporary relief. For example, Progressive offers a “Payment Arrangement” program that allows you to spread out payments over time. Allstate has a “Hardship Program” for customers facing financial difficulties.

Reinstatement Process

If your policy is canceled due to non-payment, you can usually reinstate it—but it’s not always simple. You’ll need to pay all past-due premiums, late fees, and possibly a reinstatement fee. Some insurers require you to sign a new application or agree to new terms.

In some cases, especially if the lapse was long, the insurer may treat it as a new policy. This means you could face higher rates or different coverage options.

Long-Term Financial and Legal Impacts

The effects of missing a car insurance payment don’t end when you finally pay up. There are long-term consequences that can affect your finances, driving record, and even your credit.

Credit Score Damage

If your missed payment leads to a canceled policy and unpaid bills, your insurer may send the debt to a collections agency. Once that happens, it can appear on your credit report and lower your credit score.

A lower credit score affects more than just loans—it can impact your ability to rent an apartment, get a cell phone plan, or even land a job. And since many insurers use credit-based insurance scores to set rates, a damaged credit history could mean higher premiums for years.

Difficulty Getting Coverage in the Future

Insurance companies keep records of lapses in coverage. When you apply for a new policy, they’ll see that you had a gap. This makes you a higher risk in their eyes, which can lead to higher quotes or even denial of coverage.

Some drivers end up having to go through specialty insurers that cater to high-risk drivers. These companies often charge significantly higher rates and offer fewer discounts.

Legal Liability in Accidents

If you’re involved in an accident while uninsured, you could be held personally liable for damages. This means you might have to pay out of pocket for medical bills, vehicle repairs, and other costs—potentially tens of thousands of dollars.

In some states, you could even face criminal charges, especially if the accident results in injury or death. The legal and financial fallout can be devastating.

How to Prevent Missing Payments in the Future

The best way to avoid the stress and cost of missing a car insurance payment is to prevent it from happening in the first place. Here are some practical tips to stay on track.

Set Up Automatic Payments

This is the easiest and most reliable method. By enabling auto-pay, you ensure your premium is deducted on time every month. Most insurers offer this option online or through their mobile app.

Just make sure your bank account or credit card has sufficient funds. Overdraft fees can be just as costly as late fees.

Use Calendar Reminders

If you prefer to pay manually, set reminders on your phone or calendar. Mark the due date a few days in advance, and set a second reminder on the day itself.

You can also use budgeting apps like Mint orYNAB to track bills and send alerts.

Choose a Payment Schedule That Works for You

Many insurers offer flexible payment options—monthly, quarterly, or annually. If cash flow is tight, paying annually might save you money (many companies offer discounts for full payments). But if you need smaller payments, monthly might be better.

Just be aware that monthly payments often come with service fees or interest.

Review Your Policy Regularly

Life changes—so should your insurance. If you’ve had a major life event (like a new job, move, or vehicle change), review your policy to make sure it still fits your needs and budget.

You might find you’re overpaying or underinsured. Adjusting your coverage can help you avoid financial strain.

What to Do If You’ve Already Missed a Payment

If you’ve already missed a payment, don’t panic. There are steps you can take to minimize the damage.

Contact Your Insurer Immediately

Call your insurance company as soon as possible. Explain the situation and ask about your options. Many insurers are willing to work with you, especially if it’s a one-time issue.

Be honest and polite. Customer service representatives are more likely to help if you’re cooperative.

Pay What You Can

Even if you can’t pay the full amount, send what you can. Some insurers may accept partial payments or set up a payment plan.

Every dollar you pay reduces the risk of cancellation and late fees.

Ask About Grace Periods or Hardship Programs

Don’t assume your policy is canceled. Ask if you’re still within the grace period or if there’s a hardship program available.

Some companies offer temporary relief for customers facing job loss, medical issues, or other emergencies.

Document Everything

Keep records of all communications with your insurer—emails, letters, and notes from phone calls. This can help if there’s a dispute later.

Conclusion

Missing a car insurance payment is stressful, but it’s not the end of the world. With quick action and clear communication, you can often resolve the issue and get back on track. The key is to understand the consequences, know your options, and take steps to prevent it from happening again.

Remember, your car insurance is more than just a bill—it’s a vital protection for you, your family, and others on the road. Don’t let a missed payment put that at risk. Set up reminders, use auto-pay, and stay in touch with your insurer. A little planning today can save you a lot of trouble tomorrow.

Frequently Asked Questions

Can I drive my car if I miss a payment?

No, you should not drive if your policy is canceled due to non-payment. Driving without insurance is illegal in most states and can result in fines, license suspension, or vehicle impoundment.

How long do I have to pay after missing a due date?

Most insurers offer a grace period of 7 to 15 days. During this time, your coverage remains active, but you’ll likely be charged a late fee.

Will missing one payment cancel my policy?

Not immediately. Your policy will only be canceled if you don’t pay within the grace period. However, repeated missed payments increase the risk of cancellation.

Can I get my policy back after cancellation?

Yes, most insurers allow reinstatement. You’ll need to pay all past-due amounts, late fees, and possibly a reinstatement fee. Some may require a new application.

Does a missed payment affect my credit score?

Only if the debt is sent to collections. If your insurer reports the unpaid bill to a collections agency, it can appear on your credit report and lower your score.

What if I can’t afford to pay my premium?

Contact your insurer right away. Many offer payment plans, hardship programs, or temporary relief for customers facing financial difficulties.