How Much Is Car Insurance for a 19-year-old per Month?

Contents

- 1 Key Takeaways

- 2 📑 Table of Contents

- 3 How Much Is Car Insurance for a 19-Year-Old Per Month?

- 4 Why Is Car Insurance So Expensive for 19-Year-Olds?

- 5 Average Car Insurance Costs for 19-Year-Olds by State

- 6 Factors That Influence Car Insurance Rates for Young Drivers

- 7 Ways to Lower Car Insurance Costs for 19-Year-Olds

- 8 Full Coverage vs. Minimum Coverage: What’s Right for You?

- 9 Shopping for Car Insurance: Tips for 19-Year-Olds

- 10 Conclusion

- 11 Frequently Asked Questions

Car insurance for a 19-year-old typically costs between $200 and $400 per month, but prices vary widely based on location, driving record, vehicle type, and coverage level. While young drivers face higher premiums due to limited experience, smart choices—like choosing a safe car, maintaining good grades, or bundling policies—can significantly reduce monthly costs.

Key Takeaways

- Age is a major factor: 19-year-olds are considered high-risk drivers, leading to higher insurance premiums compared to older, more experienced drivers.

- Location impacts cost: Urban areas with high traffic and crime rates often have much higher insurance rates than rural or suburban regions.

- Vehicle type matters: Sports cars and luxury vehicles cost more to insure than safe, reliable sedans or compact cars.

- Coverage level affects price: Full coverage (liability, collision, and comprehensive) is more expensive than state-minimum liability-only plans.

- Good grades can lower rates: Many insurers offer discounts for students with a B average or higher, known as the “good student discount.”

- Defensive driving courses help: Completing an approved driving course may qualify you for a discount with some insurance providers.

- Shop around and compare: Getting quotes from at least three insurers can help you find the most affordable rate for your situation.

📑 Table of Contents

- How Much Is Car Insurance for a 19-Year-Old Per Month?

- Why Is Car Insurance So Expensive for 19-Year-Olds?

- Average Car Insurance Costs for 19-Year-Olds by State

- Factors That Influence Car Insurance Rates for Young Drivers

- Ways to Lower Car Insurance Costs for 19-Year-Olds

- Full Coverage vs. Minimum Coverage: What’s Right for You?

- Shopping for Car Insurance: Tips for 19-Year-Olds

- Conclusion

How Much Is Car Insurance for a 19-Year-Old Per Month?

If you’re a 19-year-old looking to get behind the wheel—or you’re a parent helping your teen do the same—you’re probably wondering: how much is car insurance for a 19-year-old per month? The short answer? It depends. But on average, you can expect to pay between $200 and $400 per month for car insurance at this age. That’s significantly higher than what older, more experienced drivers pay, and there are good reasons for that.

Insurance companies base their rates on risk. And when it comes to young drivers, especially those under 25, the risk is higher. Statistically, teens and young adults are more likely to be involved in accidents, drive distracted, or make impulsive decisions behind the wheel. That’s why insurers charge more—they’re preparing for a higher chance of claims. But don’t let that number scare you. With the right strategies, you can lower your monthly premium and still get solid coverage.

The good news? There are plenty of ways to reduce your car insurance costs as a 19-year-old. From choosing the right car to maintaining good grades, small decisions can add up to big savings. In this guide, we’ll break down the average costs, explore the factors that influence your rate, and share practical tips to help you get the best deal possible. Whether you’re insuring your first car or adding a teen to a family policy, this article will give you the information you need to make smart, informed choices.

Why Is Car Insurance So Expensive for 19-Year-Olds?

Visual guide about How Much Is Car Insurance for a 19-year-old per Month?

Image source: forbes.com

Let’s be honest—car insurance for young drivers isn’t cheap. But why exactly does a 19-year-old pay so much more than someone in their 30s or 40s? The answer lies in data, not discrimination. Insurance companies use actuarial tables and crash statistics to determine risk, and the numbers for young drivers aren’t great.

According to the Insurance Institute for Highway Safety (IIHS), drivers aged 16 to 19 are nearly three times more likely to be in a fatal crash than drivers aged 20 and older. That risk peaks at age 16 and slowly decreases with age and experience. By 19, the risk is still significantly higher than average. This increased likelihood of accidents translates directly into higher insurance premiums.

Another factor is inexperience. Even if a 19-year-old is a careful driver, they simply haven’t had as much time behind the wheel as older drivers. They’re less familiar with handling unexpected situations—like sudden weather changes, aggressive drivers, or mechanical failures. This lack of experience makes insurers nervous, and that nervousness shows up in your monthly bill.

There’s also the issue of behavior. Young drivers are more likely to engage in risky behaviors like speeding, texting while driving, or driving under the influence. While not every 19-year-old does these things, insurers have to account for the overall trend. And let’s not forget about peer pressure—teens and young adults are more likely to drive with friends in the car, which increases distraction and accident risk.

The Role of Gender in Insurance Rates

Interestingly, gender still plays a role in insurance pricing—especially for young drivers. Historically, male drivers under 25 have been involved in more accidents than their female counterparts. As a result, 19-year-old males often pay higher premiums than 19-year-old females. However, this gap narrows significantly after age 25, and some states have even banned gender-based pricing altogether.

For example, in California, Massachusetts, and Montana, insurers cannot use gender as a factor when setting rates. In other states, the difference might be $50 to $100 per month between male and female drivers of the same age. While this may seem unfair, it’s based on long-term statistical trends. That said, as more data becomes available and driving behaviors evolve, this gap is slowly shrinking.

How Driving Record Affects Your Premium

Your driving history is one of the biggest factors in determining your insurance cost. A clean record—no accidents, tickets, or violations—can help keep your rates lower, even as a young driver. But even one mistake can cause your premium to spike.

For instance, a single speeding ticket might increase your monthly payment by $30 to $50. A DUI or at-fault accident? That could double or even triple your rate. At 19, a major violation can stay on your record for years, affecting your insurance costs long after the incident.

The good news is that time helps. As you build a clean driving history, your risk profile improves, and your rates will gradually decrease. Many insurers offer accident forgiveness programs or safe driver discounts after a few years of incident-free driving. So even if you make a mistake early on, you can recover—and save money—over time.

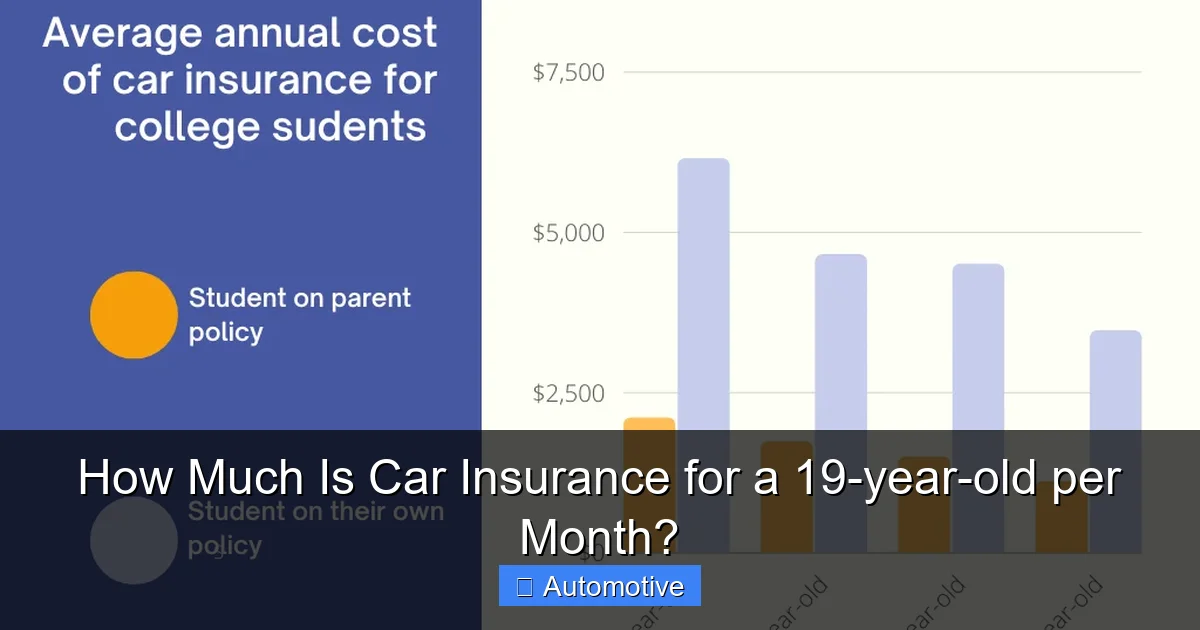

Average Car Insurance Costs for 19-Year-Olds by State

Visual guide about How Much Is Car Insurance for a 19-year-old per Month?

Image source: forbes.com

Where you live has a huge impact on how much you’ll pay for car insurance. Insurance is regulated at the state level, and each state has different requirements, traffic laws, and accident rates. That means a 19-year-old in Michigan might pay drastically more than one in Maine—even if they drive the same car and have the same record.

Let’s look at some real-world examples. In states like Michigan, which has no-fault insurance laws and high repair costs, the average monthly premium for a 19-year-old can exceed $500. In contrast, states like Maine, Ohio, or Wisconsin often have lower averages, sometimes under $200 per month.

Here’s a quick breakdown of average monthly costs for 19-year-olds in select states (based on recent industry data):

– **Michigan:** $450–$600

– **Louisiana:** $350–$500

– **Florida:** $300–$450

– **California:** $250–$400

– **Texas:** $220–$380

– **Ohio:** $180–$300

– **Maine:** $150–$250

These numbers reflect full coverage policies. If you opt for state-minimum liability only, you might pay 30% to 50% less. But keep in mind—minimum coverage often isn’t enough to protect you financially in a serious accident.

Urban vs. Rural: The Location Divide

Even within the same state, your location matters. Drivers in big cities like New York, Los Angeles, or Chicago typically pay more than those in small towns or rural areas. Why? Higher population density means more traffic, more accidents, and more opportunities for theft or vandalism.

For example, a 19-year-old in downtown Chicago might pay $400 a month, while someone in a rural part of Illinois pays $250. The difference comes down to risk. Urban areas have more stop-and-go traffic, more pedestrians, and higher rates of car theft—all factors that insurers consider when setting rates.

Parking is another issue. If you live in an apartment building with street parking, your car is more exposed to damage and theft than if you have a private garage. Some insurers even ask where you park your car overnight—because it affects your risk level.

Factors That Influence Car Insurance Rates for Young Drivers

Visual guide about How Much Is Car Insurance for a 19-year-old per Month?

Image source: thumbor.forbes.com

Now that we’ve covered the basics, let’s dive deeper into the specific factors that determine how much you’ll pay for car insurance at 19. Understanding these can help you make smarter choices and potentially lower your premium.

1. Type of Vehicle

The car you drive has a major impact on your insurance cost. Insurers look at safety ratings, repair costs, theft rates, and performance when setting rates. A high-performance sports car like a Subaru WRX or Ford Mustang will cost more to insure than a reliable sedan like a Toyota Corolla or Honda Civic.

Why? Sports cars are more expensive to repair, more likely to be stolen, and often driven more aggressively. Even if you’re a safe driver, the type of car sends a signal to insurers about your risk level.

On the other hand, vehicles with high safety ratings, advanced driver-assistance systems (like automatic emergency braking), and low theft rates can qualify for discounts. Some insurers even offer “safe vehicle” discounts for cars with features like lane departure warnings or blind-spot monitoring.

2. Coverage Level and Deductibles

The type of coverage you choose directly affects your monthly payment. Most states require at least liability insurance, which covers damage and injuries you cause to others. But liability-only plans don’t protect your own vehicle.

Full coverage—which includes collision and comprehensive—costs more but offers better protection. Collision covers damage from accidents, while comprehensive covers theft, vandalism, weather damage, and more.

Your deductible also plays a role. This is the amount you pay out of pocket before insurance kicks in. A higher deductible (like $1,000) means lower monthly payments, but you’ll pay more if you file a claim. A lower deductible (like $250) means higher premiums but less financial strain after an accident.

For a 19-year-old on a budget, a higher deductible might make sense—if you can afford to pay it if needed. Just make sure you have savings set aside for emergencies.

3. Credit Score (Where Allowed)

In most states, insurers can use your credit score to help determine your rate. The logic? People with good credit tend to file fewer claims. While this may seem unfair, studies have shown a correlation between credit history and insurance risk.

At 19, you might not have a long credit history—or any at all. That can work against you. But building good credit now can help lower your insurance costs in the future. Paying bills on time, keeping credit card balances low, and avoiding debt can all help improve your score.

Note: In California, Hawaii, and Massachusetts, insurers cannot use credit scores to set rates. So if you live in one of these states, this factor won’t affect you.

4. Annual Mileage

The more you drive, the higher your risk of an accident. Insurers often ask how many miles you drive per year. If you commute to college or work 50 miles a day, you’ll likely pay more than someone who only drives on weekends.

Some insurers offer low-mileage discounts for drivers who put fewer than 7,500 or 10,000 miles on their car each year. If you’re a student who walks or takes public transit most of the time, this could save you money.

5. Marital Status

Here’s one you might not expect: married drivers often pay less than single drivers. Insurers view married people as more responsible and less likely to take risks. At 19, most people aren’t married, so this usually doesn’t apply—but it’s something to keep in mind as you get older.

Ways to Lower Car Insurance Costs for 19-Year-Olds

Now for the good part: how to save money. Even though you’re in a high-risk category, there are plenty of ways to reduce your monthly premium. Here are the most effective strategies.

Stay on Your Parents’ Policy

One of the best ways to save is to stay on your parents’ car insurance policy—if they’re willing and able to add you. Family plans often offer multi-car discounts, and your parents’ longer driving history can help lower the overall rate.

However, this only works if you’re living at home and not using the car as your primary vehicle. If you’re away at college and have your own car, you’ll likely need your own policy.

Maintain Good Grades

Many insurers offer a “good student discount” for full-time students with a B average or higher. This can save you 10% to 25% on your premium. You’ll usually need to provide a report card or transcript as proof.

Some companies also offer discounts for students who live more than 100 miles away from home and don’t bring a car to school. If you’re commuting to campus without a vehicle, ask your insurer about this.

Take a Defensive Driving Course

Completing an approved defensive driving or driver’s education course can qualify you for a discount with many insurers. These courses teach safe driving techniques, hazard awareness, and accident prevention.

Some states even require young drivers to complete a course before getting a license. Even if it’s not required, the skills you learn can make you a safer driver—and potentially lower your insurance cost.

Choose a Safe, Affordable Car

As we mentioned earlier, the car you drive matters. Opt for a vehicle with high safety ratings, low repair costs, and a low theft rate. Avoid sports cars, luxury vehicles, and models with high insurance group ratings.

You can check insurance costs for specific models using tools from insurers or websites like the IIHS or NHTSA. A few hundred dollars in savings per year adds up over time.

Increase Your Deductible

Raising your deductible from $500 to $1,000 can reduce your monthly payment by $20 to $50. Just make sure you have enough savings to cover the higher out-of-pocket cost if you need to file a claim.

Bundle Policies

If your parents have home or renters insurance, ask if you can bundle your car insurance with their policy. Many insurers offer multi-policy discounts of 10% to 20%.

Use Telematics or Usage-Based Programs

Some insurers offer programs that track your driving habits using a smartphone app or a device plugged into your car. If you drive safely—avoiding hard braking, speeding, and late-night driving—you could earn a discount.

These programs are especially helpful for young drivers who want to prove they’re responsible behind the wheel.

Full Coverage vs. Minimum Coverage: What’s Right for You?

One of the biggest decisions you’ll make is how much coverage to buy. Let’s break down the options.

State Minimum Liability

This is the bare minimum required by law. It covers bodily injury and property damage you cause to others in an accident. But it doesn’t cover your own injuries or vehicle damage.

For a 19-year-old, this might seem like a way to save money—but it’s risky. If you’re in a serious accident, the costs can far exceed your liability limits, leaving you personally responsible for thousands of dollars.

Full Coverage

Full coverage includes liability, collision, and comprehensive. It protects you, your passengers, and your vehicle. While it costs more, it offers peace of mind—especially if you have a newer or more valuable car.

If you financed your car or are leasing it, your lender will likely require full coverage. Even if you own your car outright, full coverage is often worth the extra cost, especially in the first few years.

How to Decide

Ask yourself: Can I afford to replace my car if it’s totaled? Can I pay for major repairs out of pocket? If the answer is no, full coverage is probably the better choice.

A good rule of thumb: If your car is worth more than $4,000, consider full coverage. If it’s older or has high mileage, liability-only might be sufficient.

Shopping for Car Insurance: Tips for 19-Year-Olds

Finding the right insurance policy takes time—but it’s worth it. Here’s how to shop smart.

Get Multiple Quotes

Don’t settle for the first quote you get. Prices can vary by hundreds of dollars between insurers. Use online comparison tools or contact agents directly to get at least three quotes.

Ask About Discounts

Make a list of all the discounts you might qualify for—good student, safe driver, defensive driving, low mileage, etc.—and ask each insurer if they offer them.

Read the Fine Print

Make sure you understand what’s covered—and what’s not. Look for exclusions, limits, and claim procedures. A cheaper policy isn’t a good deal if it doesn’t protect you when you need it.

Consider Customer Service and Claims Process

Price isn’t everything. Look for insurers with good customer reviews, fast claims processing, and 24/7 support. You don’t want to be stuck on hold for hours after an accident.

Reassess Annually

Your rates can change each year based on your driving record, location, and other factors. Review your policy annually and shop around to make sure you’re still getting the best deal.

Conclusion

So, how much is car insurance for a 19-year-old per month? On average, between $200 and $400—but that number can be lower with the right choices. While young drivers face higher premiums due to age and inexperience, there are many ways to reduce costs and get quality coverage.

From choosing a safe car and maintaining good grades to shopping around and taking defensive driving courses, small steps can lead to big savings. And as you build a clean driving record, your rates will naturally decrease over time.

The key is to be proactive. Don’t just accept the first quote you get. Do your research, ask questions, and take advantage of every discount available. With the right approach, you can drive safely, stay protected, and keep more money in your pocket.

Remember, car insurance isn’t just a legal requirement—it’s a smart investment in your future. Whether you’re heading off to college, starting your first job, or just gaining independence, having the right coverage gives you peace of mind on the road.

Frequently Asked Questions

How much does car insurance cost for a 19-year-old per month on average?

The average monthly cost for car insurance for a 19-year-old ranges from $200 to $400, depending on factors like location, vehicle type, driving record, and coverage level. Full coverage tends to be more expensive than state-minimum liability plans.

Why is car insurance so expensive for 19-year-olds?

Insurance companies view 19-year-olds as high-risk drivers due to limited experience and higher accident rates. Statistics show that young drivers are more likely to be involved in crashes, which leads to higher premiums.

Can a 19-year-old get discounts on car insurance?

Yes! Many insurers offer discounts for good students, completing defensive driving courses, low mileage, safe vehicles, and bundling policies. These can significantly reduce monthly costs.

Should a 19-year-old get full coverage or just liability insurance?

It depends on the car’s value and your financial situation. Full coverage is recommended if you have a newer or financed vehicle. For older, paid-off cars, liability-only may be sufficient—but it offers less protection.

Does gender affect car insurance rates for 19-year-olds?

In most states, yes—19-year-old males typically pay more than females due to higher accident rates. However, this gap narrows with age, and some states prohibit gender-based pricing.

How can a 19-year-old lower their car insurance premium?

Ways to save include staying on a parent’s policy, maintaining good grades, choosing a safe car, increasing the deductible, taking a defensive driving course, and shopping around for the best rate.